-

Mark Verwoert

- Last updated: April 6, 2026

Educational Disclaimer: The content on myinvestacademy.com is for educational and informational purposes only. We are not licensed financial advisors, and nothing in this article should be interpreted as professional investment, legal, or tax advice. Investing involves risk of loss. Always consult with a professional before making financial decisions.

Best Dividend ETFs for 2026

Dividend ETFs have quietly outperformed the S&P 500 in early 2026. While growth stocks and the Magnificent Seven have lost ground, income-focused funds like SCHD and DVY are up on the year. With rate cuts expected and investors rotating away from high-valuation tech, dividend investing is back in focus.

This guide covers the five best dividend ETFs you can buy right now. We explain what each one does, what it costs, and who it suits. By the end, you will have a clear shortlist and know exactly how to buy one.

What Is a Dividend ETF?

An ETF (exchange-traded fund) is a basket of stocks that trades on a stock exchange like a regular share. You buy one ETF and instantly own a small slice of every company inside it. A dividend ETF is an ETF that specifically holds stocks paying regular dividends. The fund collects those dividend payments and passes them on to you, the investor, on a set schedule, usually quarterly or monthly.

This makes dividend ETFs useful for two types of investors: those who want a regular income from their portfolio, and those building long-term wealth by reinvesting those payouts over time. The key advantage over holding individual dividend stocks is diversification. If one company in the fund cuts its dividend, the impact on your income is minimal. With a single stock, a dividend cut hurts immediately.

Dividend ETFs have been outperforming the broader market lately and are thus considered one of the best ETFs to buy now.

How We Select the Best Dividend ETFs

Not every high-yield ETF is worth owning. A fund paying 10% today might be doing so by holding financially stressed companies that cut their dividends within a year. We assessed each fund on five criteria:

- Dividend yield: We look at the trailing 12-month yield and compare it to the S&P 500 average of around 1.3%. A worthwhile dividend ETF should beat that by a meaningful margin.

- Expense ratio: The annual fee charged by the fund. Lower is better. A 0.5% expense ratio on a 3% yield eats 17% of your income before you see a penny.

- Dividend history: Has the fund consistently paid and grown its distributions? We favour funds with at least five years of reliable payment history. Many of the stocks in dividend ETFs are part of the dividend aristocrats.

- Holdings quality: We check sector exposure, concentration, and the financial health of the underlying companies. High yield from low-quality stocks is a warning sign, not a feature.

- AUM and liquidity: Larger funds are more stable and easier to trade. We only included funds with significant assets under management.

Every ETF on this list was assessed in Q1 2026 based on current data.

Top 5 Best Dividend ETFs for 2026

We reviewed all dividend ETFs based on the requirements we mentioned earlier e.g. expense ratio, dividend history, AUM and more. Here is a quick comparison of all five funds before we get into the details:

ETF | Ticker | Yield (approx.) | Expense Ratio | Best For |

Schwab U.S. Dividend Equity ETF | SCHD | ~3.5% | 0.06% | Dividend growth + quality |

Vanguard High Dividend Yield ETF | VYM | ~3.1% | 0.06% | Broad diversification |

JPMorgan Equity Premium Income ETF | JEPI | ~7–9% | 0.35% | High monthly income |

Vanguard Dividend Appreciation ETF | VIG | ~1.8% | 0.06% | Long-term dividend growth |

iShares Core Dividend Growth ETF | DGRO | ~2.3% | 0.08% | Consistent dividend growers |

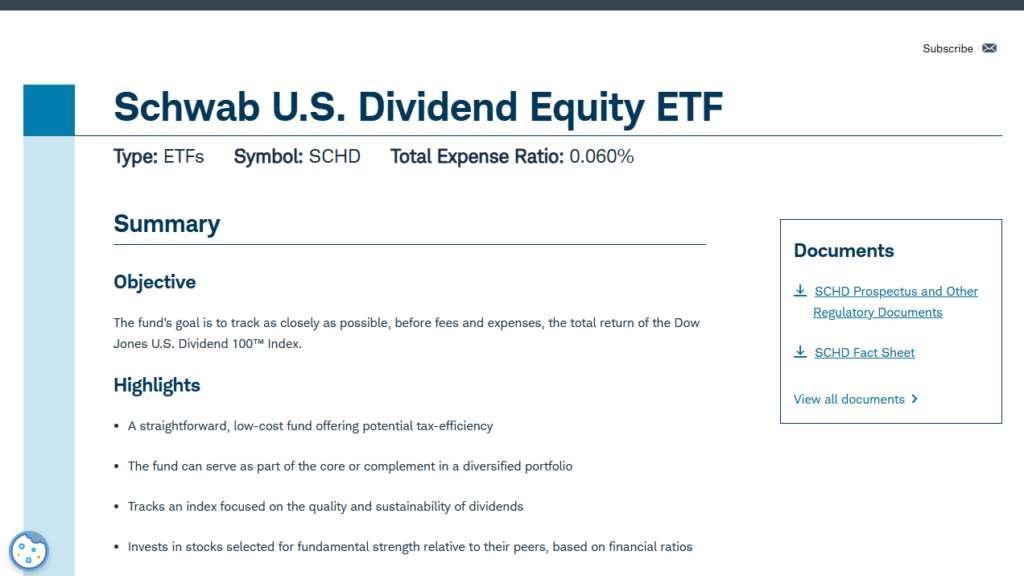

1. SCHD - Schwab U.S. Dividend Equity ETF

Ticker: SCHD | Yield: ~3.5% | Expense Ratio: 0.06% | Frequency: Quarterly | AUM: ~$65 billion |

SCHD tracks the Dow Jones U.S. Dividend 100 Index, which holds 100 U.S. companies with at least 10 consecutive years of dividend payments and strong balance sheets. Names like Chevron, Lockheed Martin, and Coca-Cola have sat in the portfolio for years.

What sets SCHD apart is its focus on quality. The index screens for cash flow to debt ratios, return on equity, and dividend yield relative to peers. This means the fund avoids chasing the highest payers and instead holds companies with the financial strength to keep paying.

The dividend growth record is particularly compelling. SCHD has delivered consistent double-digit annual dividend growth over the past decade. That means the income you receive grows every year without you doing anything.

The 0.06% expense ratio is as low as it gets. For every $1,000 invested, you pay 60 cents per year in fees.

- Best for: Long-term investors who want growing income over time, not just the highest yield today.

- Trade-off: Lower yield than JEPI. The fund has limited tech exposure, which can cause it to lag in strong bull markets driven by large-cap tech stocks.

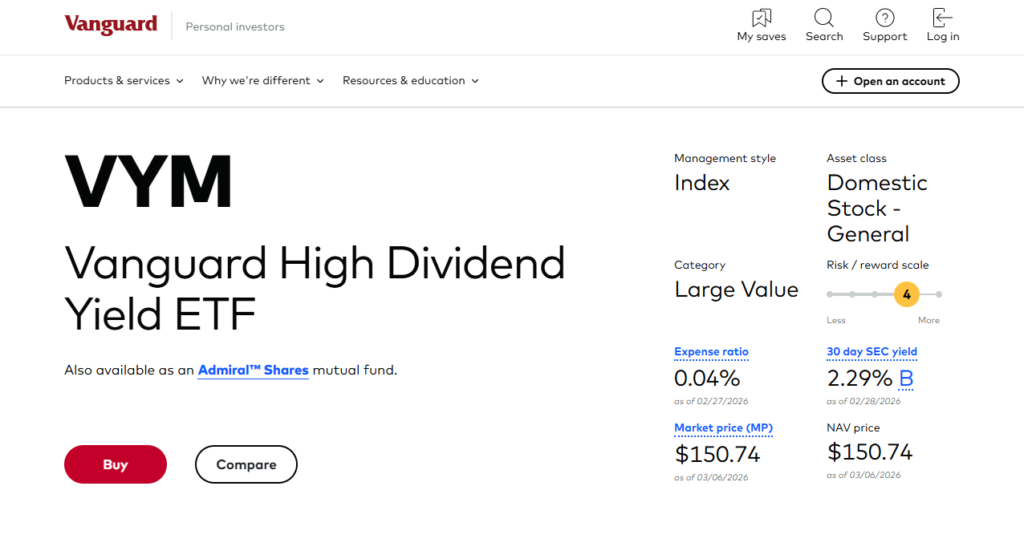

2. VYM - Vanguard High Dividend Yield ETF

Ticker: VYM | Yield: ~3.1% | Expense Ratio: 0.06% | Frequency: Quarterly | AUM: ~$60 billion |

VYM tracks the FTSE High Dividend Yield Index and holds around 500 dividend-paying U.S. stocks. That is five times more holdings than SCHD, making it the most diversified option on this list.

Top holdings include Exxon Mobil, JPMorgan Chase, and Procter & Gamble. The fund leans toward financials, healthcare, and consumer staples, sectors with historically reliable dividend payments.

Because VYM casts such a wide net, no single company dominates. The top 10 holdings account for roughly 25% of the fund, compared to over 40% in more concentrated funds.

Like SCHD, the expense ratio is just 0.06%. For a Vanguard fund, that is expected. For an income-focused ETF, it is excellent.

- Best for: Conservative investors who want maximum diversification at minimal cost. It works well as a core dividend holding alongside a growth ETF.

- Trade-off: Slightly lower yield than SCHD and less emphasis on dividend growth quality. The broad selection means you own some slower-growing dividend payers alongside the strong ones.

3. JEPI - JPMorgan Equity Premium Income ETF

Ticker: JEPI | Yield: ~7–9% | Expense Ratio: 0.35% | Frequency: Monthly | AUM: ~$40 billion |

JEPI is different from every other fund on this list. It is actively managed and uses a covered call strategy on top of a defensive stock portfolio to generate monthly income. The result is a yield of roughly 7 to 9%, paid every single month.

The fund holds 100 to 150 large-cap U.S. stocks with lower volatility than the broader market. On top of that, the managers sell covered call options on the S&P 500, collecting the option premiums and distributing them as income.

The monthly payment schedule makes JEPI particularly attractive for investors who need regular cash flow, such as retirees drawing down a portfolio.

The 0.35% expense ratio is higher than the passive ETFs on this list, but for an actively managed fund generating 7%+ in monthly income, it is still competitive.

- Best for: Retirees or near-retirees who need regular income now rather than dividend growth over time.

- Trade-off: The covered call strategy caps upside in strong bull markets. In a year where the S&P 500 is up 25%, JEPI will likely trail significantly. The yield also varies month to month.

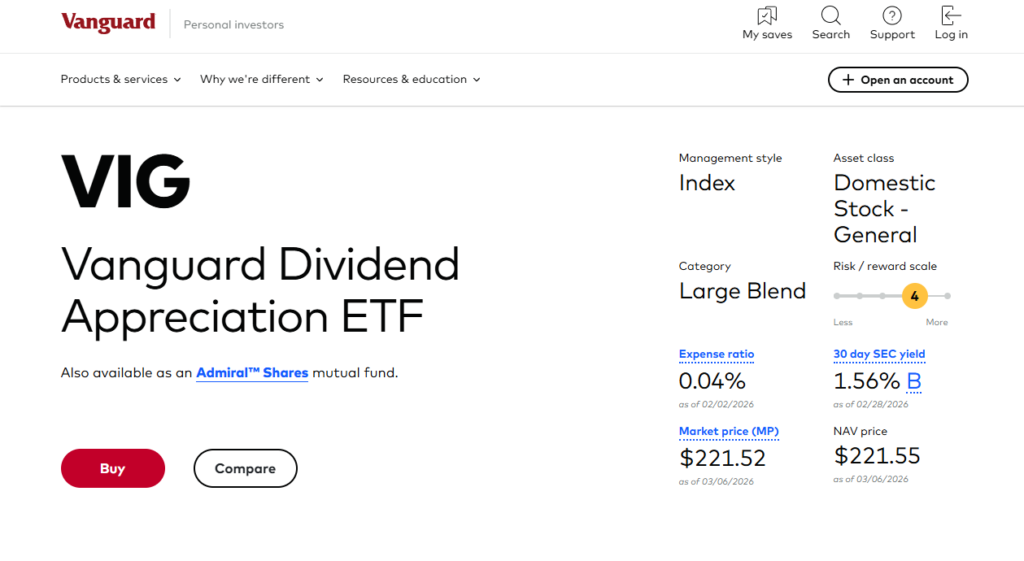

4. VIG - Vanguard Dividend Appreciation ETF

Ticker: VIG | Yield: ~1.8% | Expense Ratio: 0.06% | Frequency: Quarterly | AUM: ~$100 billion |

VIG tracks the S&P U.S. Dividend Growers Index. To be included, a company must have increased its dividend every year for at least 10 consecutive years. That strict requirement results in a portfolio of 330 high-quality businesses with proven financial discipline.

The fund has a larger tech weighting than the others on this list, with Apple, Microsoft, and Broadcom among its top holdings. This gives VIG a blend of technology growth and dividend reliability that you will not find in SCHD or VYM.

The yield is low at around 1.8%. But the point of VIG is not current income. It is building a position that pays significantly more in 15 to 20 years. An investor who bought VIG a decade ago is now receiving a much higher yield on their original investment.

- Best for: Investors with 10 or more years until retirement who prioritise long-term total return and growing income over time.

- Trade-off: The lowest yield on this list by a significant margin. Not suitable for anyone who needs income from their portfolio today.

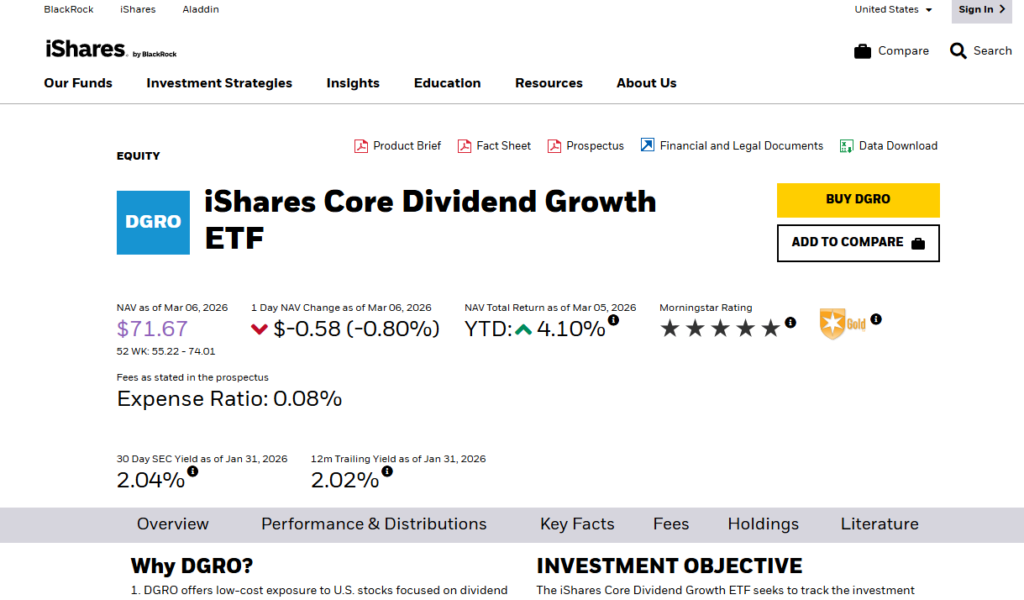

5 DGRO - iShares Core Dividend Growth ETF

Ticker: DGRO | Yield: ~2.3% | Expense Ratio: 0.08% | Frequency: Quarterly | AUM: ~$37 billion |

DGRO tracks the Morningstar U.S. Dividend Growth Index. It requires five or more consecutive years of dividend growth and, critically, filters out companies with payout ratios above 75%. That second screen matters. A company paying out most of its earnings as dividends has little room to grow them.

The result is a portfolio of over 400 stocks across financials, healthcare, technology, and industrials. It is broader than SCHD but more selective than VYM, sitting comfortably between the two.

DGRO has delivered a five-year total return of around 59%, one of the strongest on this list. That performance comes from a combination of modest yield and solid capital appreciation from its quality holdings.

- Best for: Investors who want dividend growth with wider diversification than SCHD offers. A good alternative for those put off by SCHD’s heavier sector concentration.

- Trade-off: Slightly higher expense ratio than Vanguard equivalents at 0.08%, though this is still very low. Lower yield than VYM.

Dividend Yield ETFs vs. Dividend Growth ETFs

Before choosing a dividend ETF, it helps to understand the difference between two distinct strategies: going after yield now, or building income for later.

Dividend yield ETFs (like JEPI and VYM) maximise the income you receive today. They hold high-yielding stocks and, in the case of JEPI, use options strategies to boost payouts further. They are designed for investors who need cash flow from their portfolio right now.

Dividend growth ETFs (like SCHD, VIG, and DGRO) prioritise companies that grow their dividends consistently. The yield today is lower, but in 10 to 15 years, that original investment pays significantly more. They are designed for wealth builders, not income drawers.

A practical comparison: imagine investing $10,000 in a 7% yield ETF today versus a 2% yield ETF that grows its dividend by 10% per year. After 15 years, the growth ETF is paying you more annually than the high-yield fund, and your capital has likely appreciated further too.

Neither approach is wrong. Many investors hold both. Retirees often lean toward yield ETFs. Investors still in accumulation phase typically favour growth ETFs.

For a deeper look at structuring your portfolio around income, read our guide to income investing.

How to Buy a Dividend ETF: 5 Steps

Buying a dividend ETF takes about 15 minutes once your account is set up. Here is how to do it.

Step 1: Choose a regulated stock broker

You need a brokerage account that supports ETF trading. Look for a broker that is regulated in your country, has low trading fees, and gives access to U.S.-listed ETFs if you want funds like SCHD or JEPI.

Our guide to the best stock brokers compares the top platforms by fees, features, and ease of use.

Step 2: Open and fund your account

Most brokers require identity verification (a passport or driving licence) and proof of address. The process is typically done online and takes one to two business days.

Minimum deposits vary. Some platforms have no minimum at all. Others require a few hundred pounds or dollars to start. Two popular options are:

- Interactive Brokers: low fees, broad ETF selection, suitable for more experienced investors

- eToro: beginner-friendly interface, commission-free ETF trading

Step 3: Search for the ETF by ticker

In your broker’s search bar, type the ticker symbol of the fund you want (for example: SCHD, VYM, or JEPI). Confirm you have the right fund by checking the full name and the fund issuer (Schwab, Vanguard, or JPMorgan).

If you are based outside the U.S., check whether your broker offers access to U.S.-listed ETFs or whether you need to use a European equivalent (such as an UCITS version of the fund).

Step 4: Place your order

Choose between a market order, which buys at the current price immediately, or a limit order, which only executes if the price reaches a level you set.

For most investors buying an ETF as a long-term holding, a market order placed during stock market hours works fine. Avoid placing orders before the market opens or after it closes, as spreads tend to be wider.

Step 5: Consider setting up a dividend reinvestment plan (DRIP)

A DRIP automatically uses your dividend payments to buy more shares of the same ETF, rather than paying the cash to your account. Over time, this compounds your returns significantly.

If you are in accumulation mode and do not need the income now, enabling a DRIP is one of the simplest ways to accelerate your portfolio’s growth. If you need the cash flow, skip it and let the dividends land in your account.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

Conclusion

SCHD remains our top pick for most investors in 2026. Its 0.06% expense ratio, 10-year dividend track record, and quality-focused index methodology make it hard to beat. The yield of around 3.5% is not the highest on this list, but it is backed by companies with the financial strength to keep growing it. For investors building income over time, SCHD delivers the best balance of reliability, growth, and low cost.

This guide has covered what a dividend ETF is, how to evaluate one, and five of the best options available right now. SCHD suits long-term wealth builders, VYM offers maximum diversification, JEPI delivers high monthly income, VIG targets quality dividend growers, and DGRO provides a broader middle ground. Whichever you choose, the first step is opening a brokerage account and buying your first share

Frequently Asked Questions

JEPI currently yields roughly 7 to 9%, making it the highest-paying fund on this list. However, that yield comes from a covered call strategy that caps upside in bull markets. Very high dividend yields always involve a trade-off. A 10%+ yield without an obvious strategy behind it is usually a warning sign worth investigating before investing.

Yes. SCHD remains the most recommended dividend ETF among income investors, including on platforms like Reddit's r/dividends community. Its quality-focused methodology, consistent dividend growth, and rock-bottom 0.06% expense ratio have not changed. It continues to hold financially strong companies with long dividend track records.

It depends on the fund. SCHD, VYM, VIG, and DGRO all pay quarterly. JEPI pays monthly, which is one of the reasons it appeals to retirees and income-focused investors. Always check the fund's distribution policy before investing if the payment frequency matters to you.

For equity ETFs, a yield of 2% to 4% is generally considered sustainable and healthy. The S&P 500 average sits around 1.3%, so anything above that adds meaningful income. Yields above 7% exist but require scrutiny. They are often generated through options strategies or by holding higher-risk companies. High yield without a clear explanation is worth questioning.

Yes, dividend ETFs are one of the most beginner-friendly investment options available. You get instant diversification across dozens or hundreds of companies, lower risk than picking individual dividend stocks, and a simple way to earn passive income. SCHD or VYM are sensible starting points. Both are low-cost, well-diversified, and have long track records.

Generally, yes. Dividend payments from ETFs are typically treated as taxable income. The exact treatment depends on your country of residence, the type of account you hold the ETF in, and whether there is a tax treaty between your country and the U.S. for U.S.-listed funds. Tax rules vary significantly. Speak to a tax adviser if you are unsure how dividends will be treated in your specific situation.

Both charge 0.06% and pay quarterly. VYM holds around 500 stocks and prioritises broad diversification with a slightly lower current yield of around 3.1%. SCHD holds 100 stocks, is more selective about quality, and has a stronger dividend growth track record. VYM suits investors who want maximum diversification. SCHD suits those who prioritise quality and growing income.

References

- Morningstar — Top High-Dividend ETFs for Passive Income in 2026

- (NerdWallet) — High-Dividend ETFs: What They Are and How to Choose

- (Investopedia) — Dividend ETFs vs. Dividend Stocks