-

Mark Verwoert

- Last updated: April 6, 2026

Educational Disclaimer: The content on myinvestacademy.com is for educational and informational purposes only. We are not licensed financial advisors, and nothing in this article should be interpreted as professional investment, legal, or tax advice. Investing involves risk of loss. Always consult with a professional before making financial decisions.

Best ETFs to Buy Now in 2026: Top 5 Picks for Every Investor

Over 85% of actively managed funds underperform the S&P 500 over a 10-year period. That single statistic is the argument for index ETFs in one sentence. For most investors, picking the best ETFs to buy now is not about chasing the highest returns. It is about owning the right index at the lowest possible cost and holding it long enough to matter.

In 2026, dividend stocks are outperforming growth names, international markets are drawing renewed attention, and bonds are yielding more than they have in years. That makes fund selection more interesting than usual. This guide covers five ETFs built for different goals, compares them side by side, and explains exactly how to buy one.

What Is an ETF?

An ETF, or exchange-traded fund, is a fund that holds a basket of assets and trades on a stock exchange like a single share. Buy one ETF and you instantly own a small slice of every asset inside it.

Most ETFs are passive, meaning they track a specific index rather than relying on a fund manager to pick investments. A passive S&P 500 ETF simply buys all 500 companies in that index in the same proportions. No guesswork, no active trading, no high fees.

Active ETFs do exist. A manager picks the holdings and aims to beat the market. The catch is that active management costs more, and most active managers fail to outperform their benchmark over the long run. The funds on this list are all passive, with one note on how that distinction matters when comparing costs.

ETFs can hold almost any asset class: U.S. stocks, global stocks, bonds, commodities, or sector-specific baskets. The five funds below cover the most useful categories for a long-term investor, from a simple S&P 500 tracker to a globally diversified equity fund to a bond ETF built for portfolio stability.

The two core advantages of ETFs over individual stock picking are diversification and cost. A single ETF can hold hundreds or thousands of companies. If one collapses, the impact on your portfolio is minimal. And because most ETFs simply track an index, the annual fees are a fraction of what a traditional fund manager would charge.

How We Select the Best ETFs

Not every low-cost ETF is worth buying. A fund can have a rock-bottom expense ratio and still be poorly constructed. We assess each fund on five criteria before it makes this list.

- Long-term returns: We look at the 10-year annualised total return compared to the fund’s relevant benchmark. A good ETF should track its index tightly without significant drag.

- Expense ratio: The annual cost charged by the fund as a percentage of assets. Even a 0.1% difference compounds dramatically over 20 years. On a £100,000 portfolio over 30 years, a 0.5% fee costs roughly £70,000 more than a 0.03% fee, assuming identical returns.

- Index methodology: How stocks are selected and weighted. Market-cap weighting (the most common approach) means larger companies make up a bigger share of the fund. Understanding this matters when assessing concentration risk.

- Diversification: Number of holdings, sector spread, and geographic exposure. The more genuine diversification a fund offers, the less any single event can derail it.

- AUM and liquidity: Total assets under management and daily trading volume. Larger, more liquid funds have tighter bid-ask spreads and are less likely to be closed or restructured by the issuer.

Every ETF on this list was reviewed in Q1 2026. One important note: the five funds below are not five versions of the same thing. VOO covers U.S. large-cap. QQQ targets growth and tech. VTI widens that to the entire U.S. market. VT extends it globally. BND adds bonds for stability. They serve different purposes, and the right choice depends entirely on your goals.

Best ETFs to Buy Now: Top 5 for 2026

We reviewed all ETFs based on criteria like long-term returns, expense ratio and AUM. Before we look at the detailed breakdown of our top 5 best ETFs to buy now , here is a quick side-by-side comparison before the detailed reviews:

ETF | Ticker | 10-Yr Avg Return | Expense Ratio | Best For |

Vanguard S&P 500 ETF | VOO | ~14.6% p.a. | 0.03% | Core portfolio: U.S. large-cap |

Invesco QQQ Trust | QQQ | ~17.2% p.a. | 0.18% | Growth investors: tech-heavy |

Vanguard Total Stock Market ETF | VTI | ~14.3% p.a. | 0.03% | Total U.S. market exposure |

Vanguard Total World Stock ETF | VT | ~9.8% p.a. | 0.07% | Global diversification |

Vanguard Total Bond Market ETF | BND | ~4.2% yield | 0.03% | Defensive / income allocation |

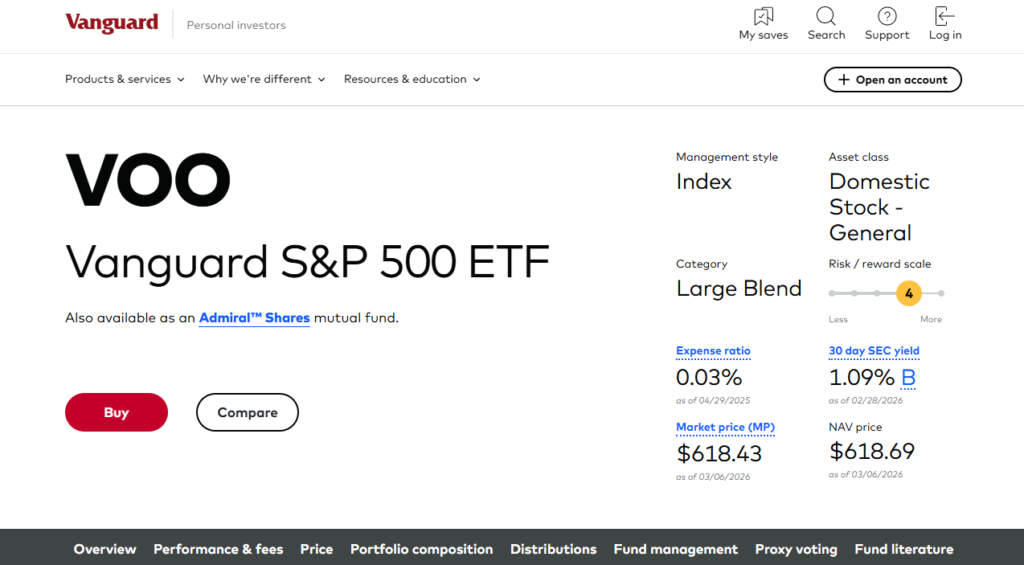

1. VOO: Vanguard S&P 500 ETF

Ticker: VOO | 10-yr avg return: ~14.6% p.a. | Expense ratio: 0.03% | AUM: ~$600 billion | Frequency: Quarterly distributions |

VOO tracks the S&P 500 index, which holds 500 of the largest publicly listed U.S. companies weighted by market capitalisation. When people talk about “the market”, they usually mean the S&P 500. Buying VOO is as close as you can get to owning the U.S. economy in a single trade.

The 0.03% expense ratio is essentially free. For every £10,000 invested, you pay £3 per year. Vanguard, which operates as a client-owned company, has consistently been the benchmark for low-cost investing. VOO has generated an average annual return of roughly 14.6% over the past decade.

Warren Buffett has publicly recommended low-cost S&P 500 index funds as the default investment for most people, including in letters to Berkshire Hathaway shareholders. His argument: over long time horizons, the S&P 500 outperforms almost everything else when you account for fees. The data backs this up. Over any given 10-year period in the past 30 years, only about 14% of actively managed funds have beaten the index.

The top 10 holdings (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, Berkshire Hathaway, Broadcom, Tesla, JPMorgan) make up roughly 33% of the fund. That concentration is worth acknowledging. VOO is not evenly spread across 500 companies. It is heavily weighted toward the largest ones.

- Best for: Any investor who wants a single core holding that captures broad U.S. market growth at minimal cost. Beginners and experienced investors alike use VOO as the backbone of their portfolio.

- Trade-off: U.S.-only exposure. If international markets outperform the U.S. over the next decade, which several major investment firms now forecast, VOO will lag a globally diversified fund. Heavy concentration in the top 10 holdings means a tech sector correction has an outsized impact. See our deeper look at the best S&P 500 ETF options if you want to compare VOO against alternatives like IVV and SPY.

2. QQQ: Invesco QQQ Trust

Ticker: QQQ | 10-yr avg return: ~17.2% p.a. | Expense ratio: 0.18% | AUM: ~$300 billion | Frequency: Quarterly distributions |

QQQ tracks the Nasdaq-100 index, which holds the 100 largest non-financial companies listed on the Nasdaq exchange. Around 65% of the fund sits in technology stocks. The top holdings are Nvidia, Apple, Microsoft, Broadcom, and Amazon. If you want concentrated exposure to the companies driving artificial intelligence, cloud computing, and semiconductor growth, QQQ delivers that in one fund.

The 10-year performance record is exceptional. QQQ has returned roughly 17.2% per year on average over the past decade, outperforming VOO by more than 2 percentage points annually. A £10,000 investment made 10 years ago would be worth over £64,000 today. QQQ has beaten the S&P 500 on a rolling 12-month basis nearly 88% of the time over the same period.

The higher expense ratio of 0.18% reflects the fact that QQQ is an older fund from Invesco rather than a client-owned operation like Vanguard. It is still cheap by any standard outside the Vanguard range. Investors who want a similar product at lower cost can consider QQQM, the newer version from Invesco designed specifically for long-term holding, which charges 0.15%.

- Best for: Growth investors with a long time horizon who are comfortable with volatility and want maximum exposure to technology and innovation.

- Trade-off: Concentration risk is significant. When tech sells off, QQQ falls harder and faster than VOO. In 2022, QQQ dropped 33% while VOO dropped 18%. That volatility is the price of the higher long-term return. QQQ also pays little in dividends, making it unsuitable for investors focused on income.

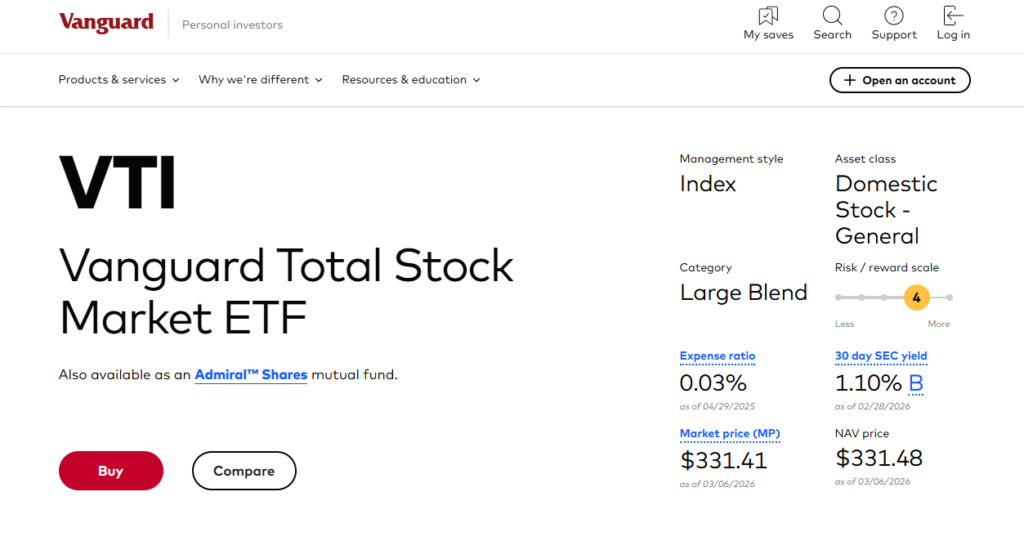

3. VTI: Vanguard Total Stock Market ETF

Ticker: VTI | 10-yr avg return: ~14.3% p.a. | Expense ratio: 0.03% | AUM: ~$450 billion | Holdings: ~3,700 stocks |

VTI tracks the CRSP US Total Market Index, which covers virtually every publicly listed U.S. company. Where VOO holds 500 large-cap stocks, VTI holds around 3,700, spanning large-, mid-, small-, and micro-cap companies. It is the most complete picture of the U.S. equity market available in a single fund.

The practical difference from VOO is smaller than it might appear. Because VTI weights holdings by market capitalisation, the largest companies still dominate. The top 10 holdings in VTI are the same companies as in VOO, and they make up a similar proportion of the fund. The 10-year return of 14.3% sits just below VOO’s 14.6%, reflecting this overlap.

Where VTI genuinely differs is in the exposure it adds below the large-cap tier. Small- and mid-cap companies have historically delivered strong returns over very long time horizons, and they represent sectors and growth stories that never reach the S&P 500. A biotech startup, a regional bank, a fast-growing industrial company: these show up in VTI but not in VOO.

Like VOO, VTI charges 0.03%. The choice between the two is largely a question of philosophy. VTI believers argue that owning the entire market, not just the largest 500 companies, is the purest form of passive investing. VOO believers point out that the performance difference is negligible and the S&P 500 is a more recognised benchmark.

- Best for: Investors who want total U.S. market exposure and prefer a ‘own everything’ approach over a large-cap-only index.

- Trade-off: Performance is very close to VOO because large-caps dominate both. The extra breadth is real but does not dramatically change returns in most market environments. If you already own VOO, switching to VTI adds very little.

4. VT: Vanguard Total World Stock ETF

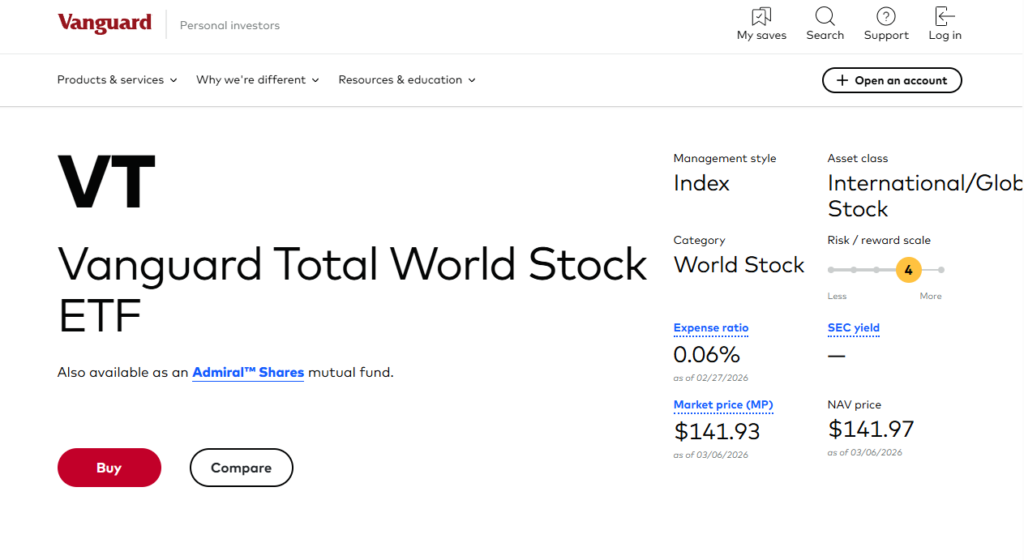

Ticker: VT | 10-yr avg return: ~9.8% p.a. | Expense ratio: 0.07% | AUM: ~$45 billion | Holdings: ~10,000 stocks across 50+ countries |

VT tracks the FTSE Global All Cap Index and holds roughly 10,000 stocks from both developed and emerging markets worldwide. U.S. stocks account for around 60% of the fund. The remaining 40% covers Europe, Japan, the UK, Canada, emerging markets, and smaller economies. It is the most diversified single-fund option on this list.

The 10-year return of 9.8% per year looks modest alongside VOO and QQQ, and it is. U.S. stocks have dominated global markets for most of the past decade, which means VT’s international exposure has been a drag on performance. But that historical gap is precisely the argument for owning it now.

Multiple major investment firms, including Morningstar, have flagged international stocks as likely to outperform U.S. markets over the next 5 to 10 years, driven by valuation differences. U.S. equities trade at significantly higher price-to-earnings multiples than European or emerging market peers. If that gap narrows, VT will benefit in a way that VOO and VTI will not. The cost is just 0.07%, which works out to roughly £7 per year on a £10,000 investment, making it one of the cheapest ways to access 10,000 global companies at once.

Investors who already hold VOO or VTI and want to add international exposure without buying a separate fund often use VT as a complete replacement rather than a complement.

- Best for: Investors who want genuine global diversification and are not comfortable concentrating their entire portfolio in the U.S. market.

- Trade-off: Lower returns over the past decade due to international underperformance. Currency risk adds a layer of volatility that a U.S.-only fund avoids. The bullish case for international stocks is a forecast, not a guarantee.

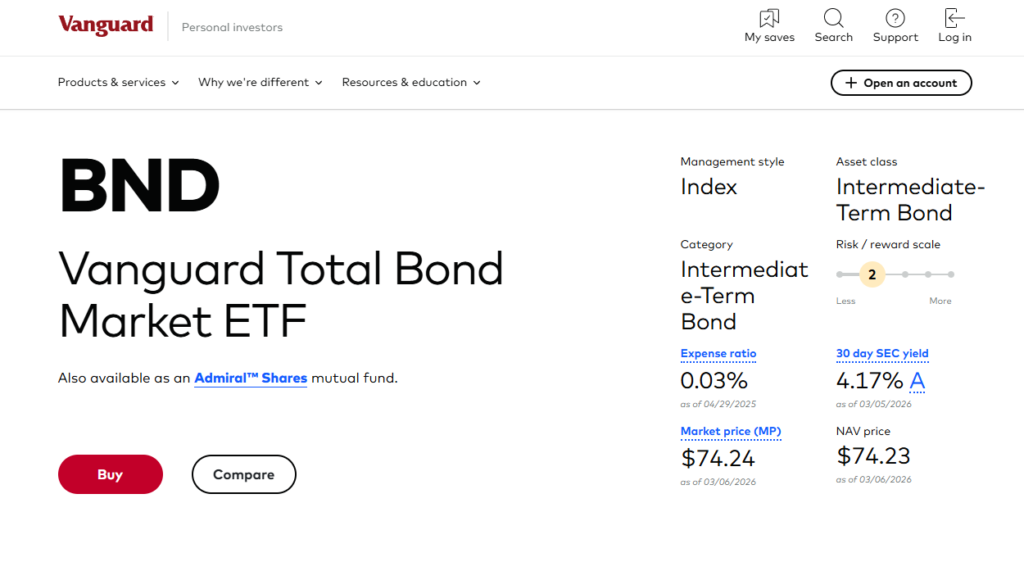

5. BND: Vanguard Total Bond Market ETF

Ticker: BND | 30-day SEC yield: ~4.2% | Expense ratio: 0.03% | AUM: ~$120 billion | Frequency: Monthly distributions |

BND tracks the Bloomberg U.S. Aggregate Float Adjusted Index and holds over 10,000 U.S. investment-grade bonds. The portfolio spans U.S. government bonds (around 45%), mortgage-backed securities, and investment-grade corporate bonds. It pays monthly income, currently yielding around 4.2% on a 30-day SEC basis.

BND is not a growth investment. Over any long time horizon, equities will outperform bonds. The role of BND in a portfolio is to reduce volatility and provide stable income. In 2022, when VOO fell 18% and QQQ fell 33%, BND fell just 13% and then recovered while paying monthly income throughout. That cushioning effect is what bonds are for.

With rate cuts expected in 2026, bonds have become more attractive than they were during the high-rate environment of 2022 to 2024. As interest rates fall, existing bonds with higher fixed yields become more valuable, which pushes bond prices up. BND investors benefit from both the monthly income and potential price appreciation if rate cuts materialise as forecast.

The 0.03% expense ratio is the lowest available for a total bond market fund. For income-focused investors who want something beyond equity dividends, BND is a straightforward option. For a more targeted approach to income from equities, take a look at our guide to the best dividend ETFs, which covers funds like SCHD and JEPI alongside their trade-offs.

- Best for: Investors approaching retirement, those building a 60/40 stock-bond portfolio, or anyone who wants to reduce overall portfolio volatility without moving to cash.

- Trade-off: Not a growth investment. In strong equity bull markets, BND will significantly underperform. Rising interest rates also hurt bond prices. BND fell in 2022 alongside equities, which surprised investors who expected bonds to act as a pure safe haven.

How to Choose the Right ETF for You

The most common question from new investors is not ‘what is a good ETF?’ but ‘which one should I actually buy?’ There is no single correct answer, but there is a straightforward framework.

- If you want one fund and nothing else: VOO or VTI. Both track the U.S. market at near-zero cost. The performance difference over the long run is negligible. VOO is simpler; VTI is slightly broader. Either works as a lifetime core holding.

- If you want higher growth and can tolerate higher volatility: Add QQQ alongside VOO or VTI. QQQ has outperformed the S&P 500 over the past decade, but it does so with more severe drawdowns. It is not a replacement for VOO; it is a complement for investors who want extra tech and growth exposure.

- If you want global diversification: Replace VOO or VTI with VT, or hold VT alongside a U.S.-only fund. VT’s international allocation reduces the risk of betting entirely on the U.S. market continuing to lead, which many forecasters now consider a stretched assumption.

- If you want to reduce volatility or generate income: Add BND. The classic 60/40 portfolio (60% equities, 40% bonds) has produced strong risk-adjusted returns over decades. As you approach retirement, increasing your bond allocation via BND smooths out the ride.

- If income from equities is the primary goal: A general ETF like VOO or VTI is not optimised for income. Dividend-focused funds serve that purpose better. Funds like SCHD, VYM, and JEPI are built specifically for investors who want regular cash distributions from their equity holdings.

Most investors do not need more than two or three ETFs. A beginner might start with VOO alone. An investor 10 years from retirement might hold VOO, BND, and VT. Overcomplicating a portfolio with 10 different ETFs rarely improves returns and adds unnecessary complexity.

The passive versus active debate is largely settled. Decades of data consistently show that low-cost passive funds outperform most actively managed alternatives after fees. The exception is in some niche markets where active management adds genuine value, but for core equity and bond exposure, passive wins.

How to Buy an ETF: 5 Steps

The process takes about 15 minutes once your account is open. Here is what to do.

Step 1: Choose a regulated broker

You need a brokerage account that supports ETF trading and gives access to U.S.-listed funds. Look for a platform that is regulated in your country, charges low trading fees, and allows fractional shares if you want to start with a smaller amount.

Our guide to the best stock broker options compares the top platforms by fees, regulation, and ease of use, and highlights which are best suited to beginners versus experienced investors.

Step 2: Open and fund your account

Most brokers require identity verification before you can trade. You will need a government-issued ID (passport or driving licence) and proof of address. The process is done online and usually takes one to two business days.

Minimum deposits vary by platform. Some have no minimum at all. Two well-established options worth considering:

- Interactive Brokers: low fees, wide range of U.S. ETFs, suitable for investors who want more advanced tools alongside simple index investing

- eToro: beginner-friendly interface, commission-free ETF trading, easy to navigate for first-time investors

Step 3: Search for the ETF by ticker

In your broker’s search bar, type the ticker symbol of the fund you want: VOO, QQQ, VTI, VT, or BND. Confirm you have the right fund by checking the full name and the fund issuer before placing an order.

If you are based outside the U.S., check whether your broker offers access to U.S.-listed ETFs or whether you need to use a UCITS equivalent. Many of these funds have European versions. For example, Vanguard FTSE All-World UCITS ETF (VWRP) is the European equivalent of VT, and iShares Core S&P 500 UCITS ETF (CSPX) mirrors VOO for European investors.

Step 4: Place your order

You have two main order types. A market order buys immediately at the current price. A limit order only executes if the price reaches a level you set. For most investors buying a broad ETF as a long-term holding, a market order placed during exchange hours works perfectly well.

Avoid placing orders outside of market hours. The New York Stock Exchange and Nasdaq are open Monday to Friday, 9:30 a.m. to 4 p.m. Eastern Time. Outside those hours, bid-ask spreads widen and you may get a worse price than expected.

Step 5: Set up a regular contribution

Dollar-cost averaging means investing a fixed amount at regular intervals regardless of the current price. It is one of the most effective strategies for long-term ETF investors. You automatically buy more shares when prices are low and fewer when prices are high. Over time, this tends to produce better average entry prices than trying to time the market.

Most brokers allow you to set up automated recurring purchases. Set a monthly amount, pick your ETF, and the platform handles the rest. For passive investors, this turns ETF ownership into a fully hands-off process.

One option to consider if you receive dividend payments: rather than drawing them as cash, you can choose to have them reinvested automatically. This is separate from dollar-cost averaging. It just means your dividend payouts buy additional shares rather than sitting in your account.

Conclusion

VOO is the top pick for most investors in 2026. At 0.03% per year, it is as cheap as investing gets. It tracks the most widely followed equity benchmark in the world, has returned roughly 14.6% per year over the past decade, and requires zero ongoing management. For a beginner building their first portfolio or an experienced investor who wants a reliable core holding, a low-cost S&P 500 ETF held for decades remains one of the most consistently effective long-term strategies available.

This guide has covered what an ETF is, how to evaluate one, and five funds built for different purposes. VOO for U.S. core exposure. QQQ for growth and technology. VTI for the broadest possible U.S. market coverage. VT for global diversification. BND for stability and income. None of them requires active management, market timing, or specialist knowledge. Pick the one that fits your goal, set up a regular contribution, and get out of your own way. The first step is opening a brokerage account.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions

Frequently Asked Questions

For most investors, VOO is the default answer. It tracks the S&P 500, costs 0.03% per year, and has returned roughly 14.6% annually over the past decade. If you want global diversification rather than U.S.-only exposure, VT is the alternative. If income is the priority, a dividend ETF is more appropriate than a broad market fund. The right answer depends on your goal.

QQQ has produced higher returns over the past decade: roughly 17.2% per year versus 14.6% for VOO. But it carries more risk. In 2022, QQQ fell 33% against VOO's 18% decline. QQQ also has a higher expense ratio (0.18% versus 0.03%) and is concentrated heavily in technology. VOO is more diversified, lower cost, and less volatile. For most investors, VOO is the safer long-term choice. QQQ suits those who want greater tech exposure and are comfortable with deeper drawdowns.

VOO or VTI. Both track the U.S. market, cost 0.03% per year, and require no active management. They hold hundreds or thousands of companies, so a single bad investment cannot sink your portfolio. Either works as a starting point. Once you are comfortable with how ETFs behave, you can decide whether to add global exposure via VT or a bond allocation via BND.

As little as the price of one share. VOO trades at roughly $500 to $600 per share as of early 2026. VTI is similar. However, many brokers now offer fractional shares, which means you can invest as little as $1 or $10 and own a proportional slice of the ETF. Check whether your broker supports fractional ETF purchases before assuming you need a full share price to get started.

ETFs carry less single-company risk than owning individual stocks. If one company inside an ETF fails, its impact on the overall fund is limited by how many other holdings the fund has. VOO, for example, holds 500 companies, so no single failure is catastrophic. That said, ETFs are not risk-free. They still fall when their underlying market falls. A total market ETF will not protect you from a broad equity selloff.

VOO tracks the S&P 500, which holds the 500 largest U.S. companies. VTI tracks the total U.S. market, holding around 3,700 stocks including small- and mid-cap companies that VOO excludes. Both cost 0.03% per year. Because large-cap stocks dominate both funds by weighting, their performance over time is very similar. VTI is slightly broader; VOO is more focused on the largest companies. If you already own one, switching to the other adds little practical difference.

U.S. ETFs like VOO and VTI have significantly outperformed global ones over the past decade, which makes them look like the obvious choice. But that outperformance was driven in part by expanding valuation multiples that now look stretched compared to international peers. Multiple major investment firms, including Morningstar, have projected that international stocks are likely to outperform U.S. stocks over the next 5 to 10 years. VT covers both in one fund. Many investors hold a U.S. ETF and VT together to maintain domestic weighting while adding international exposure.

Yes, and most investors benefit from holding two or three. A simple and widely used combination is a U.S. equity ETF (VOO or VTI) for growth, plus BND for stability. Adding VT gives global exposure without needing to buy separate regional funds. Where it gets counterproductive is owning 10 or 15 ETFs that overlap significantly. Three well-chosen ETFs built for different purposes will outperform a cluttered portfolio of overlapping funds every time.

References

- Morningstar) – Best Active ETFs to Buy in 2026

- (Kiplinger) – Best ETFs to Buy for 2026 and Beyond

- (Investopedia) – Exchange-Traded Fund (ETF): How to Invest