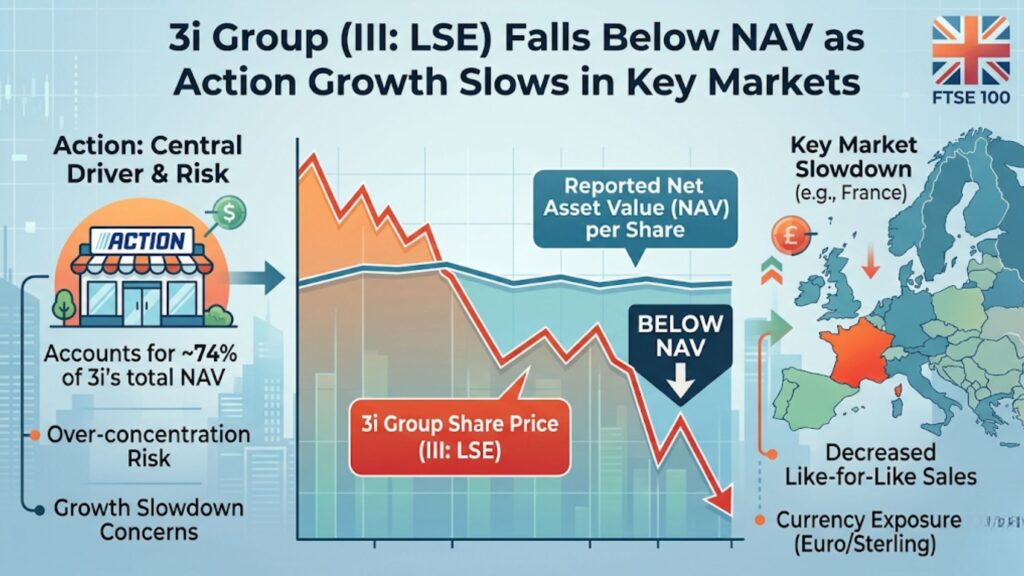

3i Group (III: LSE) Falls Below NAV as Action Growth Slows in Key Markets

3i Group PLC (III: LSE), the FTSE 100 private equity and infrastructure investor, has seen its share price fall to approximately 2,967p, placing it below its reported net asset value (NAV) per share of 3,017p for the first time in several years. The stock has declined roughly a third from its all-time high of 4,497p, reached in October 2025.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, or professional advice. Always perform your own due diligence before making any financial decisions.

Action Remains the Central Driver

The performance of 3i’s portfolio is largely determined by a single holding: Action, a European non-food discount retailer in which 3i now holds a 65.3% equity stake following a transaction with GIC in January 2026. Action accounts for approximately 74% of 3i’s total NAV.

For the 52 weeks to 28 December 2025, Action reported net sales of €16 billion and operating EBITDA of €2.37 billion, representing year-on-year growth of 16% and 14% respectively. The retailer added a record 384 net new stores during the year, bringing its total footprint to 3,302 locations across 14 countries. All stores are reported to be profitable, and early 2026 trading showed like-for-like sales growth of 6.1% in the first four weeks of January.

3i values its Action stake using a run-rate EBITDA of €2.63 billion at a multiple of 18.5 times, net of a liquidity discount, producing a carrying value of approximately £23.4 billion for its current 65.3% stake.

NAV Growth Trajectory and Current Discount

3i’s NAV per share has risen from 2,085p in March 2024 to 3,017p by December 2025, an increase of approximately 45% in under two years. The company has historically traded at a premium to NAV of as much as 65% in recent years. The current position, at a roughly 1.7% discount to reported NAV, represents a notable shift in market sentiment.

At 31 December 2025, 3i held cash of £995 million, with total liquidity of £2.2 billion including an undrawn revolving credit facility.

3i Group Valuation Debate

The appropriateness of the 18.5 times EBITDA multiple applied to Action is a point of active debate among market participants. Supporters of the methodology point to Action’s continued store expansion, with a long-term target of more than 4,850 locations compared to the current 3,302, as well as consistent new store profitability and weekly customer volumes averaging 21.6 million throughout 2025.

Critics, including short-seller ShadowFall Capital, have argued that Action is overvalued relative to European non-food retail peers and that 3i’s heavy concentration in a single asset increases risk to shareholders if growth decelerates.

Key Risks Facing the Business

Concentration in Action remains the most significant risk factor. A reduction in the valuation multiple from 18.5 times to 15 times would reduce the carrying value of the Action stake by an estimated £5 billion, bringing NAV per share down to approximately 2,420p.

France, Action’s largest market, recorded mid-single-digit like-for-like sales declines in October and November 2025, before returning to flat in December and modest growth of 2.1% in the first period of 2026. Currency exposure also presents a headwind: with Action generating revenue in euros and 3i reporting in sterling, a 1% move in the euro-sterling exchange rate translates to a net return movement of approximately £228 million.

The broader private equity portfolio, valued at roughly £7.9 billion and including holdings such as Royal Sanders, Audley Travel, and Evernex, faces limited near-term realisation opportunities given continued illiquidity in private equity markets.

3i (III:LSE) Analyst Positioning

The average analyst 12-month price target for 3i Group currently stands at 4,207p, with a range of 3,000p to 5,200p. Nine of eleven analysts covering the stock hold a buy recommendation.