PetroTal Corp. (TAL: TSX) Reserves Update Takes on New Relevance as Oil Prices Climb Sharply

When PetroTal published its year-end reserves report in late February, the headline story was a sharp fall in asset values driven by a weak oil price outlook. Less than three weeks later, the oil market looks considerably different.

Reserves Report Was Built on a $63 Oil Assumption. Brent Is Now Near $99.

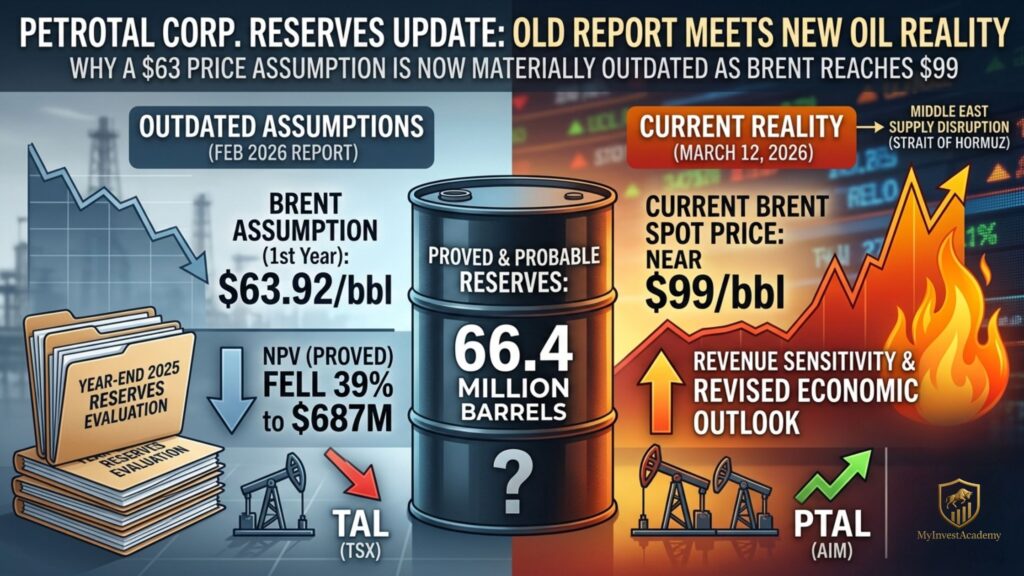

PetroTal Corp. (TSX: TAL) (AIM: PTAL) (OTCQX: PTALF) released its 2025 year-end reserve evaluation on February 25, 2026, prepared by independent evaluator Netherland, Sewell & Associates, Inc. The report showed total Proved reserves of 66.4 million barrels of oil, broadly unchanged year-on-year, while the estimated after-tax net present value of those reserves fell 39% to $687 million for the Proved category, and 32% to $1.17 billion on a Proved and Probable basis.

The primary reason for those valuation declines, as stated by the company, was a reduction in the oil price assumptions applied by its evaluator. The five-year average Brent crude price forecast used in the 2025 report was $72.23 per barrel, with a first-year assumption of just $63.92. The report was filed when Brent was trading in a range broadly consistent with those projections.

As of the morning of March 12, 2026, Brent crude reached approximately $98.76 per barrel, a level more than 50% above the first-year price assumption embedded in PetroTal’s reserve valuations. The U.S. Energy Information Administration has noted that Brent settled at $94 per barrel on March 9, up approximately 50% from the start of the year and the highest since September 2023, attributing the rise to a fall in petroleum shipments through the Strait of Hormuz and shut-ins of some Middle East oil production.

What Triggered the Move

The Strait of Hormuz, through which approximately 20% of global oil demand typically transits, has been severely disrupted following US-Israeli military strikes on Iran and Iran’s subsequent threats to target vessels attempting to use the waterway. In response, IEA member countries agreed to release 400 million barrels of oil from emergency reserves, described as the largest such release in history, in an effort to offset the disruption. Despite that intervention, prices have continued to move higher amid ongoing uncertainty about supply flows from the region.

The EIA forecasts Brent will remain above $95 per barrel over the next two months, before falling below $80 in the third quarter of 2026 and toward $70 by year end, though it notes this forecast is highly dependent on the duration of the Middle East conflict and resulting production outages.

Why This Matters for PetroTal

PetroTal’s revenues are generated entirely from the sale of crude oil produced at its Bretaña field in Peru, making the company’s financial performance directly sensitive to the Brent price. The reserve valuation figures published in the February report were calculated using a price deck that is now materially below prevailing spot prices. Investors should note that reserve valuations are point-in-time estimates and do not automatically update when commodity prices move.

The company’s share price on the TSX has reflected the changed environment. TAL stock has risen approximately 21% over the past month and approximately 11% over the past week as of March 12, 2026, though it remains down around 20% over the prior twelve months. On the AIM market in London, PTAL was last quoted at 27.50p to 28.00p as of the close on March 9, 2026.

The company’s earnings date is reported as March 19, 2026, which will provide investors with a more complete picture of how operations and cash flows developed through the fourth quarter of 2025 under the lower price environment that prevailed for most of that period.

Drilling Resumption Planned for October 2026

PetroTal did not conduct any development drilling in 2025. According to the company’s press release, the revised Bretaña field development plan now incorporates 37 production wells and nine water disposal wells in the Proved case, up from a smaller inventory at year-end 2024. Future development costs for the Proved category rose 178% to $534 million, reflecting that expanded plan.

Management indicated that drilling is planned to resume in October 2026, with the pace of investment described as adjusted in response to lower commodity prices at the time of the report. Should current oil prices prove durable, the economics supporting that development program could shift considerably. The company’s independent evaluator maintained original oil in place at the Bretaña field at 494 million barrels on a Proved and Probable basis, unchanged from year-end 2024.